Executive Summary

The current “Mediation Stasis” has created an artificial market plateau that masks deep structural risks. This advisory provides investors with the intelligence layer required to navigate high-entropy markets. By applying the UTM to capital allocation, we identify why traditional ESG and lagging economic indicators are currently providing a false sense of security in the energy and industrial sectors.

Key Takeaways

- Risk-Adjusted Energy ROI: Value has shifted from resource ownership to Transit Security and regional supply-chain autonomy.

- The Cyber-Physical Balance Sheet: A firm’s SCADA and infrastructure resilience is now a primary driver of its long-term valuation.

- Narrative Volatility: Cognitive warfare can wipe out equity value in hours; investors must account for “Narrative Resilience” in corporate leadership.

- Antifragile Rebalancing: Capital must be reallocated toward sectors that provide tech-sovereignty and critical domestic defense infrastructure.

The Fallacy of Market Resilience

In the current fiscal quarter, global equity markets have demonstrated a superficial “resilience,” with major indices trading near all-time highs despite the collapse of U.S.-Iran mediation and the ongoing fallout from Operation Epic Fury. This decoupling of market price from geopolitical reality is not a sign of stability; it is a symptom of Institutional Myopia.

Traditional investment advisories rely on lagging economic indicators and ESG (Environmental, Social, and Governance) frameworks that are fundamentally ill-equipped to account for sub-threshold state aggression, grey-zone conflict, and the weaponization of maritime chokepoints. At CommandEleven, we maintain that capital allocation in 2026 requires a transition from “Passive Exposure” to “Intelligence-Driven Active Management.”

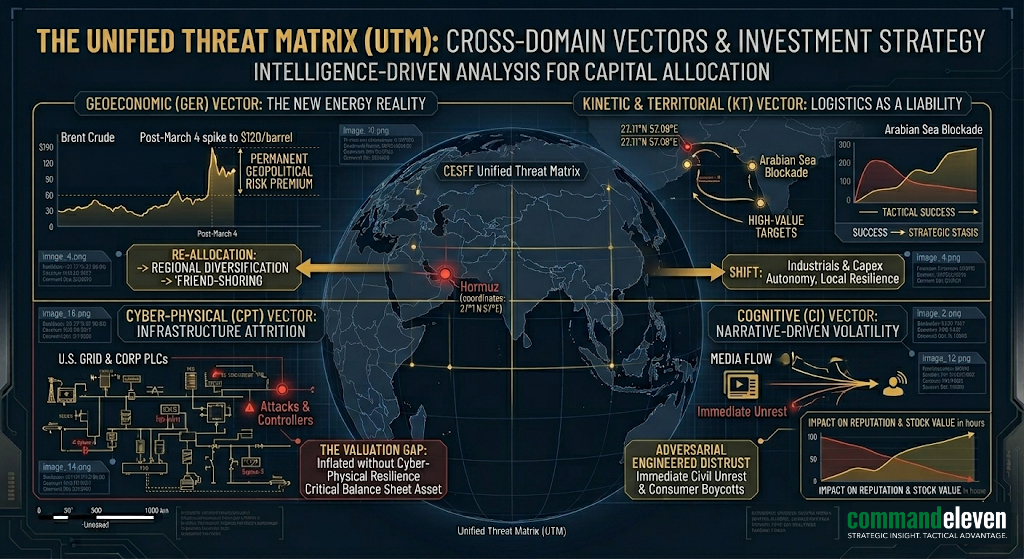

The Unified Threat Matrix (UTM) in Capital Markets

To achieve a true risk-adjusted ROI, investors must view their portfolios through the lens of the Unified Threat Matrix (UTM). The current “Mediation Stasis” has created specific distortions across the four primary vectors:

Geoeconomic (GER) Vector: The New Energy Reality

The closure of the Strait of Hormuz on March 4, 2026, and the subsequent declaration of force majeure by QatarEnergy, did more than just spike Brent Crude past $120/barrel. It established a permanent “Geopolitical Risk Premium” in global energy pricing.

- The Investment Shift: Investors must move away from broad energy ETFs and toward firms that facilitate Regional Diversification and “Friend-Shoring” of logistics. The value is no longer in the resource itself, but in the security of its transit.

Kinetic & Territorial (KT) Vector: Logistics as a Liability

Operation Epic Fury has demonstrated that “tactical success” often triggers “strategic stasis.” The subsequent Arabian Sea blockade and the domestic aerial siege of U.S. bases have turned traditional logistics hubs into operational liabilities.

- Capital Reallocation: We are seeing a decisive shift toward Industrials and Capex-linked sectors that provide autonomous, local, or resilient supply chain infrastructure. Logistics firms that lack military-grade C2 (Command and Control) integration are now high-risk assets.

Cyber-Physical (CPT) Vector: Infrastructure Attrition

The explosion of Iranian and Russian cyber-attacks on the U.S. electric grid and corporate PLCs (Programmable Logic Controllers) is a pre-positioning move for a wider conflict.

- The Valuation Gap: Corporate valuations that do not explicitly account for “Cyber-Physical Resilience” are inflated. In 2026, a firm’s SCADA system security is as critical to its balance sheet as its cash flow.

Cognitive (CI) Vector: Narrative-Driven Volatility

Adversarial “Engineered Distrust” campaigns,leveraging incidents like the Minab school strike,can trigger immediate civil unrest and consumer boycotts, impacting corporate reputation and stock value in hours.

Moving from Prediction to Preparation

The fundamental shift required for investors is moving from trying to predict a specific geopolitical outcome to preparing for a range of plausible, high-impact scenarios.

| Strategy Phase | Actionable Priority |

| Observation | Utilize “Geopolitical Radar” to monitor sub-threshold signals (e.g., shifts in regional maritime insurance or Dark Web chatter). |

| Orientation | Break institutional “Normalcy Bias.” Assume that JIT (Just-In-Time) logistics are compromised for the foreseeable future. |

| Action | Rebalance portfolios toward firms with Antifragile supply chains and those providing critical national security technology (AI, Biotech, Defense). |

Conclusion: The New “Washington Consensus”

The era of laissez-faire globalization has been replaced by a structural era of State Interventionism and Tech Sovereignty. In this environment, policy, not price, determines competitiveness.

Investors who rely on standard financial advisors are currently flying blind. CommandEleven’s Geopolitical Advisory provides the missing layer of strategic intelligence required to navigate the “Forced Convergence” of 2026. Volatility is not a risk to be feared; it is a signal for capital reallocation. The rewards will go to those who can translate intelligence into a disciplined, risk-adjusted strategy before the next cascade begins.

Note: This article is for informational purposes only and does not constitute financial advice. For bespoke regional risk assessments, contact CommandEleven’s Strategic Advisory team.