Executive Summary

This assessment deconstructs the UAE’s strategic exit from OPEC on May 1, 2026, identifying it as the terminal rupture of the Riyadh-Abu Dhabi energy alliance. Driven by a $150 billion investment in ADNOC’s production capacity and the kinetic imperatives of the 2026 Iran War, Abu Dhabi has pivoted toward a bilateral security and financial axis with Washington and Tel Aviv. By securing a $20 billion US Treasury dollar swap and rejecting the “OPEC Scarcity” model, the UAE has effectively insulated its economy from Saudi-led hegemonic corrections. The resulting “Total War” for market share signals the collapse of GCC unified energy policy and the emergence of a new, high-velocity energy hegemony in the Gulf.

3 Key Takeaways

- The Monetization Mandate: ADNOC’s move to unleash 1.5 million bpd of “shut-in” capacity is a race against the energy transition, prioritizing immediate national solvency over the cartel’s price-floor requirements.

- The Washington-Tel Aviv Pivot: The exit is backstopped by a critical $20B US Treasury liquidity injection and an intelligence-kinetic shield from Israel, providing the UAE with the financial and physical security to bypass the Saudi-centric orbit.

- Terminal GCC Fragmentation: The Saudi-Emirati “Price War” represents a geofinancial divorce that renders legacy GCC energy cooperation obsolete, shifting the regional power balance toward competitive bilateralism and independent swing production.

Primary Strategic Drivers: The Trifecta of Autonomy

The interconnectivity of the UAE’s drivers is rooted in a shift from market-preservation to resource-acceleration. For decades, the UAE operated within the Saudi-led consensus of “price stability,” sacrificing immediate revenue for the long-term health of the cartel. However, by 2026, the delta between the UAE’s internal economic requirements and OPEC’s restrictive quotas reached a breaking point. The transition is driven by a realization that in a world rapidly pivoting toward energy transition, “oil in the ground” is a depreciating asset. Abu Dhabi has determined that its sovereign survival depends on exhausting its reserves at maximum velocity before the “Peak Demand” window closes permanently.

The Production Capacity Paradox: The Monetization Sprint

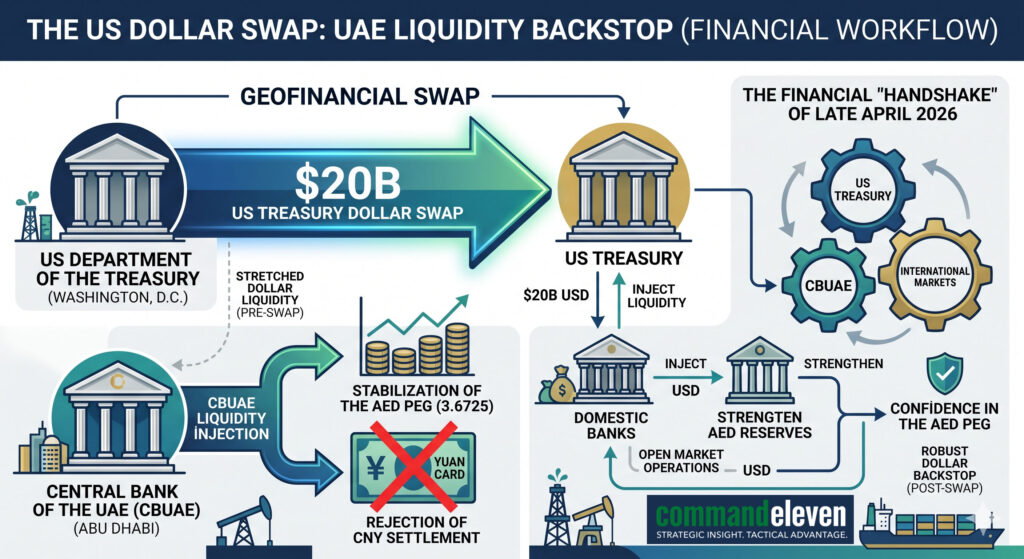

The UAE’s primary driver is the massive, $150 billion investment into ADNOC (Abu Dhabi National Oil Company) intended to expand production capacity.

- The Revenue Leak: As of 2026, ADNOC’s operational capacity stands at 4.85 million bpd, yet OPEC+ quotas have consistently capped production at approximately 3.2 million bpd. This leaves over 1.6 million bpd of “shut-in” capacity,essentially idling billions of dollars in infrastructure.

- The ROI Mandate: Unlike the legacy model of maintaining “spare capacity” as a geopolitical tool, the 2026 UAE model views spare capacity as a failed return on investment. By exiting OPEC, Abu Dhabi immediately unlocks an estimated $45B to $60B in annual revenue that was previously “sacrificed” to support the fiscal breakeven prices of less efficient OPEC members. This capital is the lifeblood for “Operation 300bn,” the UAE’s massive industrial diversification strategy.

The “Iran War” Catalyst: Recalibrating for Kinetic Disruption

The ongoing conflict in the Middle East has fundamentally altered the risk-reward calculus of cartel membership.

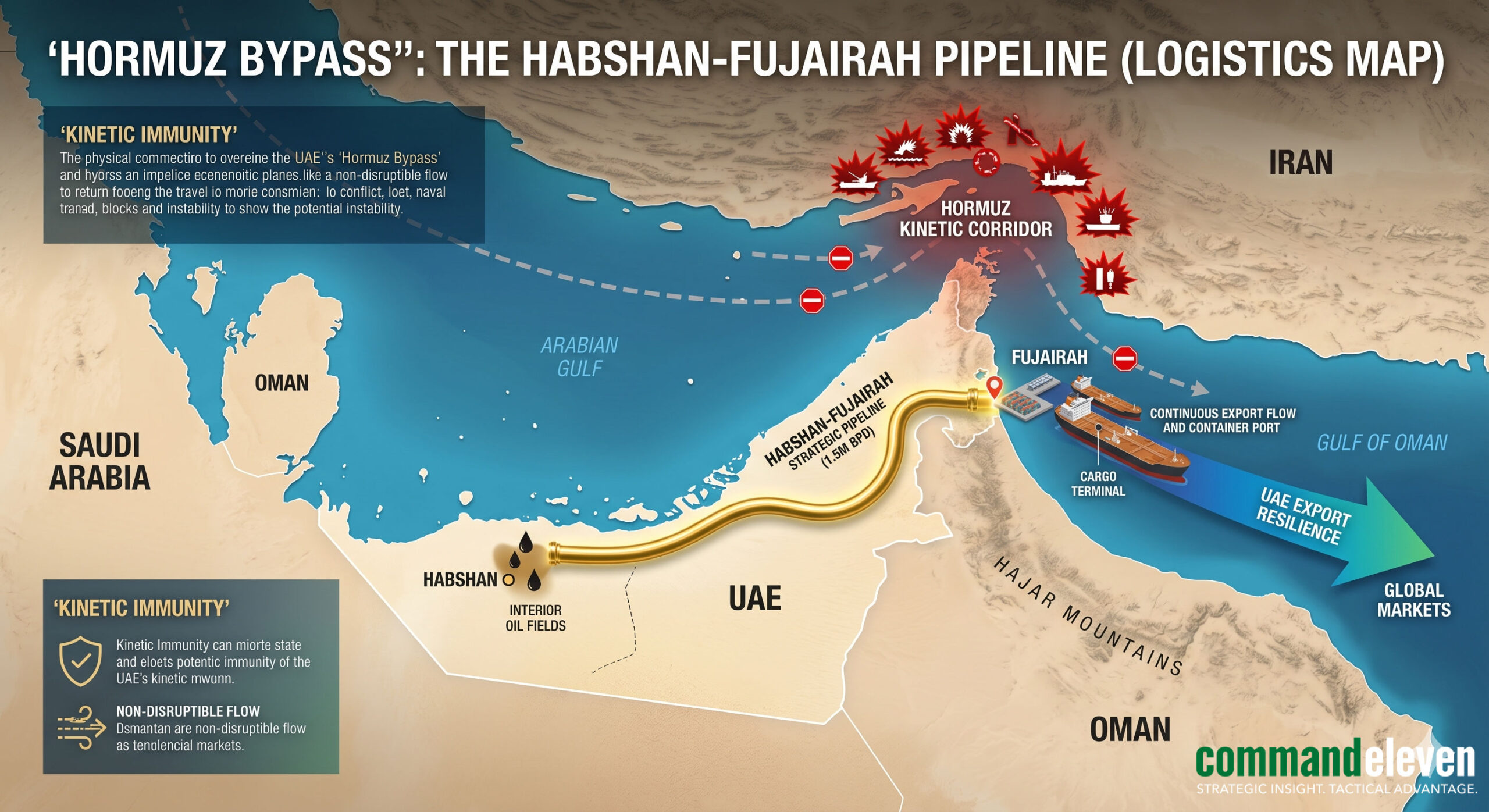

- The Hormuz Egress Crisis: With the Strait of Hormuz functioning as a high-risk “Kinetic Corridor,” the UAE’s exports have been throttled by insurance premiums and physical threats. While Saudi Arabia has shifted volume to its East-West pipeline to the Red Sea, the UAE’s Habshan-Fujairah pipeline (bypassing Hormuz) has become its primary, and at times only, viable export route.

- The Post-Conflict Surge: Abu Dhabi assesses that the current war-induced “artificial” price floor will eventually collapse once regional shipping lanes normalize. By severing ties with OPEC now, the UAE positions itself to “flood the market” the moment the kinetic threat subsides, recapturing market share lost during the blockade. They are choosing to be the “First Mover” in a post-war price war, rather than being bound by Saudi-led “Gradualism” while their market share is eaten by US and Brazilian producers.

Economic Divergence: SWFs vs. The Barrel

A critical, often overlooked driver is the fundamental divergence in how the UAE and Saudi Arabia view global growth.

- The “Demand Destruction” Threshold: Saudi Arabia requires a high price floor (~$85-$95) to fund its “Vision 2030” domestic giga-projects. In contrast, the UAE’s economy is deeply integrated into global logistics, aviation, and finance via its Sovereign Wealth Funds (ADIA, Mubadala).

- The Portfolio Conflict: When OPEC forces high oil prices during a period of global inflation, it triggers “Demand Destruction” and high interest rates, which directly devalues the UAE’s multi-trillion dollar global investment portfolios. Abu Dhabi has concluded that a moderate, stable oil price that fuels global GDP growth is more beneficial to its total national wealth than a high oil price that triggers a global recession. By leaving OPEC, they have effectively chosen the “Global Growth” side of the ledger over the “Price Fixer” side.

The Washington-Tel Aviv-Abu Dhabi Axis: A New Energy Hegemony

The interconnectivity of this driver is found in the Abraham Accords matured into a kinetic and financial defense pact. While Saudi Arabia has attempted to maintain a “balanced” posture between East and West, Abu Dhabi has gone “all-in” on a western-aligned security architecture. This axis is built on three critical pillars: the US Dollar Backstop, the Israel Intelligence/Kinetic Shield, and the Pax Silica Integration.

The US Treasury and the “Dollar Swap” Backstop

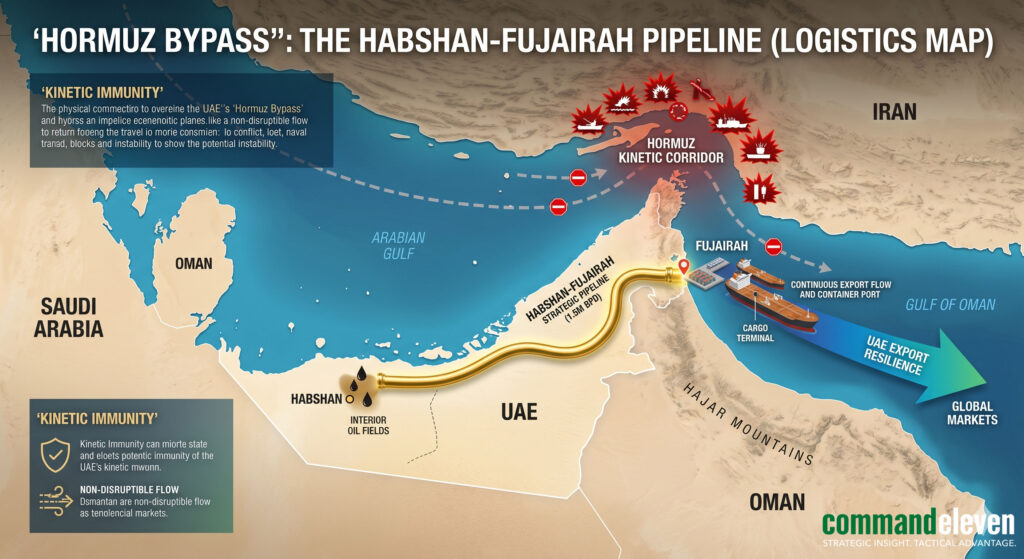

The timing of the OPEC exit was surgically aligned with US Treasury Secretary Scott Bessent’s endorsement of a $20 billion emergency dollar swap line for Abu Dhabi.

- Financial Sovereignty: In the wake of the 2026 Iran conflict and the subsequent volatility of the Dirham (AED), Abu Dhabi required a massive greenback liquidity injection to maintain its dollar peg.

- The “Yuan Card” Leverage: Abu Dhabi utilized the threat of pricing oil in Yuan (CNY) as leverage to secure this swap. By exiting OPEC, the UAE has effectively accepted a “Preferred Economic Partner” status with Washington, ensuring that its oil flows are a pillar of dollar-dominance rather than a tool for cartel-driven price spikes that harm the US economy.

The Tel Aviv Intelligence & Kinetic Shield

The UAE-Israel relationship has transformed from a diplomatic novelty into a functional survival mechanism.

- The Iron Dome/Arrow Integration: Following the massive drone and missile barrage from Iran (over 2,200 units intercepted in early 2026), the UAE has become a primary customer and integration node for Israeli-developed air defense systems.

- Intelligence-for-Oil: In exchange for the UAE’s withdrawal from the OPEC bloc – which weakens the regional leverage of Israel’s primary adversary, Iran – Tel Aviv has shared high-fidelity intelligence on IRGC maritime movements. This synergy allows the UAE to maintain production and export safety even when the Strait of Hormuz is functionally closed, utilizing Israeli-secured “Safe Corridors” in the Eastern Mediterranean and Red Sea via the Eilat-Ashkelon pipeline bypass.

Pax Silica and the Tech-Energy Convergence

The January 2026 signing of the Pax Silica Declaration by the UAE is the final piece of the puzzle. This US-led framework aims to build secure, innovation-driven supply chains for foundational technologies like AI and semiconductors.

- The AI-Energy Nexus: Abu Dhabi is currently building the world’s largest AI campus outside the US (a five-gigawatt facility). This requires massive, cheap, and reliable energy abundance – the exact opposite of the “scarcity” model enforced by OPEC.

- Strategic Decoupling: By aligning with the Pax Silica framework, the UAE has decoupled its future from the “Cartel of the Past.” It is betting that its role as a global technology hub – powered by its own unrestricted energy production – is more vital to its 2030 survival than maintaining a seat at the table in Riyadh.

Technical & Market Impacts: The Saudi-Emirati Price War

The UAE’s departure transforms OPEC from a price-setting cartel into a fractured battlefield. The market is now entering a period of “Competitive Volume,” where the primary objective for both Riyadh and Abu Dhabi is no longer a $90 barrel, but the absolute capture of Asian demand. This shift triggers a series of market shockwaves that will redefine the Brent and Murban crude benchmarks for the next decade.

The ADNOC Production Surge: “Unleashing the Murban”

With the administrative shackles of OPEC removed, ADNOC is prepared to pivot from “compliance” to “saturation.”

- Immediate Volume Injection: ADNOC has the technical capacity to add 1.2 million bpd to the global market within 90 days. This is not “paper barrels”; this is high-quality, light-sweet Murban crude that directly competes with American WTI and Saudi Arab Light.

- The “Murban” Benchmark Dominance: By flooding the market, Abu Dhabi aims to establish the IFAD (ICE Abu Dhabi Futures) Murban contract as the primary price discovery mechanism for the East-of-Suez market, effectively stripping Saudi Arabia of its ability to set Official Selling Prices (OSPs) for Asian refiners.

The “Total War” for Market Share

The fully expected Saudi-Emirati Price War will be characterized by a “Race to the Bottom.”

- Riyadh’s “Shock and Awe” Protocol: Historically, when challenged, Saudi Arabia utilizes its massive spare capacity to crash prices, intending to bankrupt higher-cost competitors. However, the UAE’s fiscal breakeven is significantly lower than Saudi Arabia’s ($55 vs $82). Abu Dhabi is betting it can outlast a price war that Riyadh initiated.

- The Asian Term-Contract Battle: We anticipate both nations offering unprecedented discounts and “loyalty rebates” to Chinese, Indian, and South Korean refiners. This is a scorched-earth policy: every barrel of Emirati crude that lands in Ningbo is a direct subtraction from the Saudi “Vision 2030” treasury.

The Brent Crude Death Spiral (May 2026 Projections)

- May 1 (The Rupture): Brent is projected to “Flash-Crash” from the war-premium highs of $110+ down to $88.00/bbl as the cartel floor vanishes.

- May 15 (The Basement): As Saudi and Emirati barrels begin to flood Asian storage hubs, Brent is expected to plummet toward the $58.00–$62.00/bbl range. This creates a “Global Stimulus” for Western importers but a catastrophic funding gap for Riyadh.

Backgrounder: The Saudi “Hegemonic Correction”

To understand the current UAE-Saudi rupture, one must examine the blueprint Riyadh has used to enforce regional submission. Saudi Arabia’s leadership is built on a “Carrot and Stick” framework intended to ensure that no GCC or Arab state operates outside the Riyadh-centric orbit.

The Qatar Blockade (The Blueprint for Coercion)

The 2017-2021 blockade of Qatar serves as the primary historical example of Saudi-led collective punishment. By severing land, air, and sea links, Riyadh attempted to force Doha to align its foreign policy with the Saudi-UAE axis. While the blockade eventually ended, it left a permanent template for how Riyadh deals with “Independent” regional actors.

Kuwait and the Neutral Zone Leverage

Kuwait has historically maintained a precarious neutrality within the GCC. Saudi Arabia has frequently utilized the Divided Zone (Neutral Zone) oil fields as a leverage point. By unilaterally shutting down production in shared fields (Khafji and Wafra) under the guise of technical or environmental concerns, Riyadh has historically “chastised” Kuwaiti leadership whenever they drifted too far toward a pro-Iran or independent diplomatic stance.

The Syrian Re-entry: “Normalization at a Price”

The recent re-admission of Syria into the Arab League was a Saudi-orchestrated move designed to sideline the UAE’s early diplomatic lead in Damascus. By taking control of the “Normalization” file, Riyadh effectively forced Bashar al-Assad to look to Saudi Arabia for reconstruction capital, ensuring that Syria’s return to the Arab fold happened on Saudi terms, not Emirati ones.

The UAE Paradox: Why the “Blueprint” Failed

The UAE watched the submission of Qatar and Kuwait and drew a different conclusion: Economic and Kinetic Independence is the only shield. Unlike Kuwait, the UAE has the military-industrial complex to push back; unlike Qatar, the UAE has a global financial footprint that Riyadh cannot easily blockade. The exit from OPEC is the UAE’s declaration that it is no longer susceptible to the “Hegemonic Correction” that has historically silenced its neighbors.

Geopolitical Second-Order Effects: The Collapse of GCC Unity

The UAE’s departure from OPEC on May 1, 2026, is not an isolated policy shift; it is the final result of a cascading regional crisis. The systemic collapse of the GCC’s unified energy stance is the byproduct of an existential economic divergence triggered by the 2026 Iran War, a desperate play for financial solvency via Washington, and a total rejection of the Riyadh-centric status quo.

The War Dividend: $120 Billion in Vanishing Wealth

The US-Israel war with Iran has dealt a near-fatal blow to the UAE’s “diversified” economic model.

- The Non-Oil Attrition: While the closure of the Strait of Hormuz on March 4, 2026, throttled oil exports, the impact on the UAE’s “Jewel in the Crown” – the logistics, tourism, and financial sectors – has been catastrophic. Since February 28, the Dubai and Abu Dhabi stock markets have shed $120 billion in value, with benchmark indexes plunging up to 16%.

- The Logistics Trap: Dubai International Airport, the world’s busiest for international transit, has seen tens of thousands of flight cancellations. For an economy where travel and tourism contribute 13% of GDP (~$70 billion), the “Surveillance Void” and kinetic threat environment have turned a global hub into a regional cul-de-sac.

The Washington “Bailout” and the Yuan Ultimatum

The most clinical driver of the UAE’s break from the GCC was the clandestine request for a $20 billion US Dollar Swap Line in late April 2026.

- The Liquidity Crisis: Despite holding over $250 billion in reserves, the UAE faced a sudden liquidity squeeze as the Iran war disrupted the financing of trade across the MENA region. The Central Bank of the UAE was forced to inject $8 billion into the domestic banking system just to maintain operational continuity.

- The Breakaway Pivot: To secure this swap line from US Treasury Secretary Scott Bessent, Abu Dhabi utilized a high-stakes “China Card.” Emirati officials warned that without a dollar backstop to preserve the Dirham peg, they would be forced to settle oil transactions in Petroyuan.

- The Trade-Off: This request was not a plea for help, but a renegotiation of terms. By securing a bilateral financial tether to Washington, the UAE gained the fiscal confidence to leave the “safety” of the OPEC/GCC collective, realizing that Riyadh could no longer provide the dollar liquidity or kinetic protection required to survive the 2026 shock.

The “Sense-Share-Contribute” Failure

The GCC’s Unified Energy Policy was built on the principle of collective production restraint to maintain prices. This model collapsed because the “Sense” of the market changed:

- Asymmetric Suffering: While Saudi Arabia utilized its East-West pipeline to mitigate the Hormuz closure, the UAE bore the brunt of Iranian missile and drone attacks,over 2,800 units targeted the UAE since the war began.

- The Debt Recall: The UAE’s sudden demand for a $3.5 billion debt repayment from Pakistan in April 2026 signaled a country aggressively clawing back capital to fund its own reconstruction and defense.

- The Final Break: Abu Dhabi concluded that the GCC “Unified” policy was merely a mechanism for Saudi Arabia to manage its own fiscal breakeven ($82/barrel) while the UAE’s economy was being physically and financially dismantled. By exiting OPEC and the GCC energy framework, the UAE has effectively declared that national solvency outweighs regional solidarity.

The Post-GCC Reality: Bilateral Hegemony

The GCC is now a “Cooperation Council” in name only. The UAE has replaced the regional collective with a Bilateral Defense and Energy Pact with the US and Israel.

- The New Axis: The UAE is betting that a Washington-backed, unrestricted production model will allow it to rebuild its infrastructure faster than the lumbering, quota-bound Saudi machine.

- The “Toll” on Unity: As the UAE ramps up production to recapture the $60 billion in “lost” annual revenue, the Saudi-Emirati “Price War” will functionally ensure that a unified GCC energy policy can never be reconstituted.

Market Watch: The Brent Crude Death Spiral (April – May 2026)

Benchmark Focus: Brent Crude (ICE) / Murban (IFAD)

Risk Vectors: Cartel Fragmentation, Price War Attrition, Geofinancial Decoupling

April 20, 2026: The “Pre-Rupture” Peak

- Brent Spot Price: $104.50 / bbl

- Market Sentiment: High-Entropy Scarcity.

- Technical Status: Prices are sustained by the “War Premium.” With the Strait of Hormuz partially obstructed and Iranian infrastructure under constant kinetic pressure, the market is pricing in a long-term supply deficit.

- The Catalyst: Clandestine reports begin to circulate regarding Abu Dhabi’s $20B US Treasury swap line. The market misinterprets this as a simple liquidity play, failing to see it as the “exit fee” for OPEC.

- CommandEleven Assessment: The “War Premium” is a hollow shell. Smart money begins to move into short positions as the UAE’s ADNOC quietly prepares to move from “Standby” to “Max-Export” mode.

May 1, 2026: The Day of the Rupture

- Brent Spot Price: $88.20 / bbl (Down 15.6% in 24 hrs)

- Market Sentiment: Structural Shock.

- The Event: Effective 00:00 GST, the UAE formally exits OPEC and OPEC+. Within minutes, ADNOC issues a revised Official Selling Price (OSP) for Murban crude, undercutting Saudi Arab Light by $4.50 per barrel.

- The “Flash-Crash”: Algorithmic trading triggers a massive sell-off as the “Cartel Floor” vanishes. The UAE announces an immediate production increase of 800,000 bpd, bypasses the Strait of Hormuz via the Fujairah pipeline, and signs a direct “Preferred Supply” contract with a consortium of South Korean and Japanese refiners.

- Saudi Response: Riyadh initiates “Operation Desert Flood.” To punish Abu Dhabi’s “betrayal,” the Saudi Ministry of Energy removes all production caps, signaling a target of 12.5M bpd. The Saudi-Emirati Price War is now a hot conflict.

May 15, 2026: The “Basement” Projection

- Brent Spot Price (Projected): $58.00 – $62.00 / bbl

- Market Sentiment: Decisive Attrition.

- Technical Status: The market has entered a “Race to the Bottom.” Both Riyadh and Abu Dhabi are prioritizing Market Share over Margin.

- The Impact of the UAE “Bailout”: Because the UAE secured its $20B US backstop, it can withstand $60 oil for longer than Saudi Arabia, whose fiscal breakeven remains trapped above $80.

- Supply Glut Reality: By mid-May, the global market is oversupplied by an estimated 3.5M bpd. Storage facilities in Fujairah and Singapore reach 95% capacity.

- The Geopolitical Pivot: US WTI (West Texas Intermediate) follows the downward trend, providing a massive “Economic Stimulus” to the Western economy at the direct expense of GCC unity. The Brent-Murban spread tightens to near-parity, signaling the end of Saudi Arabia’s role as the “Central Bank of Oil.”

Final Market Outlook

The “Price War” of May 2026 is fundamentally different from 2020. This is not a dispute over quotas; it is a geofinancial divorce.

- Winners: Highly diversified, energy-importing economies (India, Japan, South Korea) and the UAE’s tech-heavy “Pax Silica” projects.

- Losers: Saudi Arabia’s Vision 2030 (now facing a catastrophic funding gap) and high-cost producers in the North Sea and Canadian Oil Sands.

CommandEleven Risk Rating: ULTRA-HIGH. We anticipate significant political instability within the GCC as Riyadh attempts to utilize non-oil “Hegemonic Corrections” (sanctions or border closures) to force the UAE back into submission.