Executive Summary

As of May 2026, the BRICS bloc has transitioned from a consultative forum into a formalized engine of global financial fragmentation. Under India’s 2026 Chairship, the group,now expanded to eleven full members,has prioritized the operationalization of an “execution-led” economic framework. Central to this shift is the institutionalization of the mBridge platform for wholesale Central Bank Digital Currency (CBDC) settlements, which allows for cross-border trade without reliance on the US dollar or the SWIFT messaging system. CommandEleven Intelligence assesses that this expansion signals a terminal shift away from the post-1945 Bretton Woods hegemony, as the bloc creates a parallel, “sanction-proof” financial architecture. While internal rivalries,particularly between India and China,persist, the collective drive toward strategic autonomy is successfully bifurcating global capital markets.

3 Key Takeaways

- Institutionalized De-dollarization: The transition of the mBridge project from a pilot to a functional settlement rail marks the first viable, large-scale alternative to Western-dominated financial messaging, enabling sovereign local currency trade.

- Strategic Multi-Alignment: The expansion to include major energy producers like Saudi Arabia and the UAE grants the bloc unprecedented control over global capital flows, allowing members to hedge against Western economic coercion while maintaining diverse trade links.

- Fragmentation of Global Governance: The rise of BRICS+ as a functional economic pole is diminishing the relevance of the G20, as global decision-making silos into two distinct regulatory and financial systems,the G7 and the expanded BRICS.

Introduction

As of May 2026, the BRICS bloc has transitioned from a consultative forum into a formalized engine of global financial fragmentation. Under India’s 2026 Chairship, the group,now expanded to eleven full members,has prioritized the operationalization of an “execution-led” economic framework. This includes the institutionalization of the BRICS Bridge (or mBridge) for wholesale Central Bank Digital Currency (CBDC) settlements and the expansion of the “Partner Country” category to include ten additional emerging markets. CommandEleven assesses that this expansion signals a terminal shift away from the post-1945 Bretton Woods hegemony, as the bloc creates a parallel, “dollar-light” financial architecture that insulates its members from Western sanctions and G7-led economic coercion.

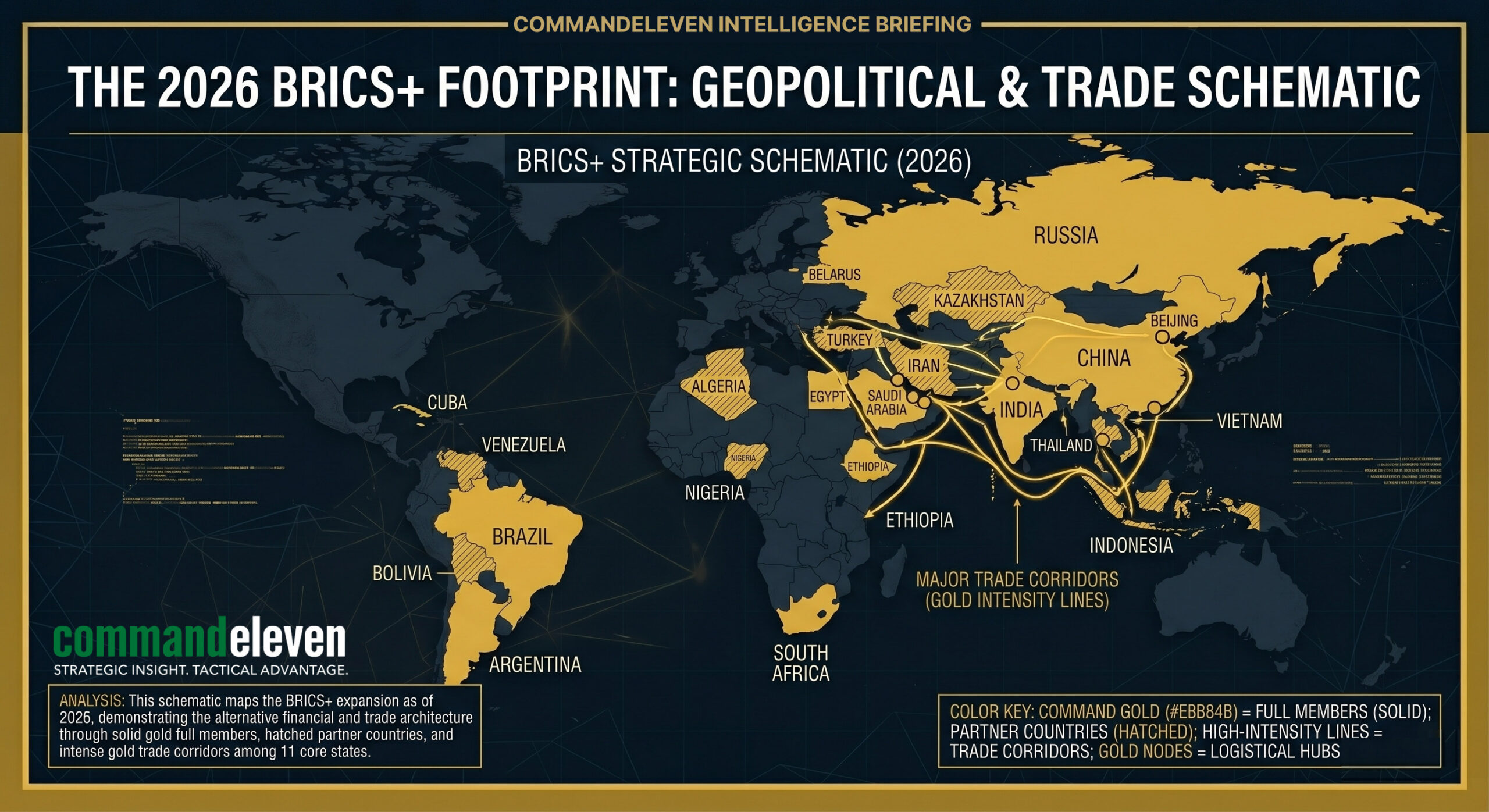

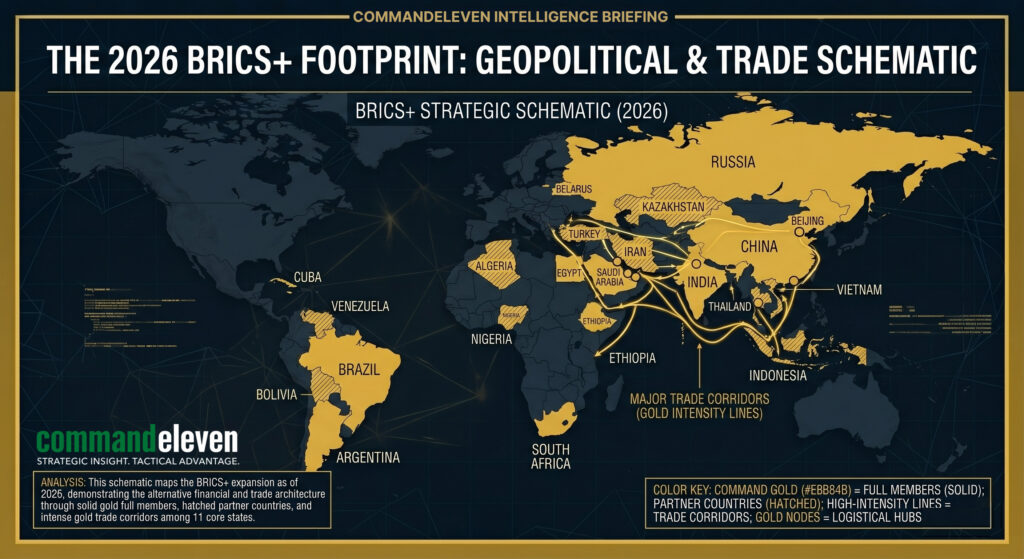

The New BRICS+ Architecture: Membership and Partnership

The 2026 landscape reflects a tiered membership structure designed to maintain consensus while expanding geopolitical reach.

- Full Members (11): Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Iran, Saudi Arabia, the United Arab Emirates (UAE), and Indonesia. Decisions are made strictly by consensus among these core states.

- Partner Countries (10): Belarus, Bolivia, Kazakhstan, Cuba, Malaysia, Nigeria, Thailand, Uganda, Uzbekistan, and Vietnam. These states participate in trade and investment initiatives but lack full voting rights on bloc-wide security and political expansion.

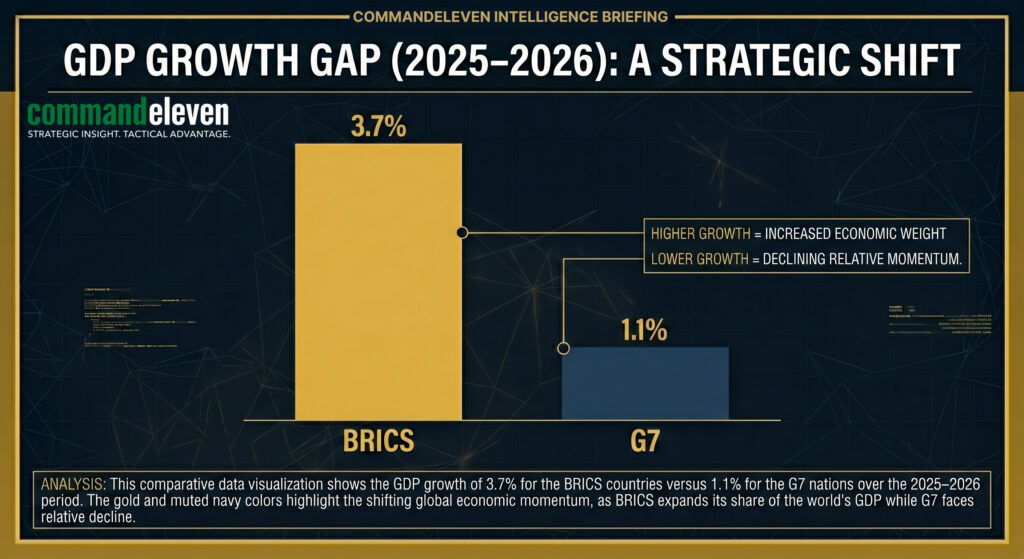

- Growth Projections: In 2026, BRICS members are projected to average 3.7% economic growth, significantly outpacing the G7 average of 1.1%. India (6.2%) and China (4.2%) remain the primary engines, while the inclusion of the UAE and Saudi Arabia provides the bloc with unprecedented control over global energy capital.

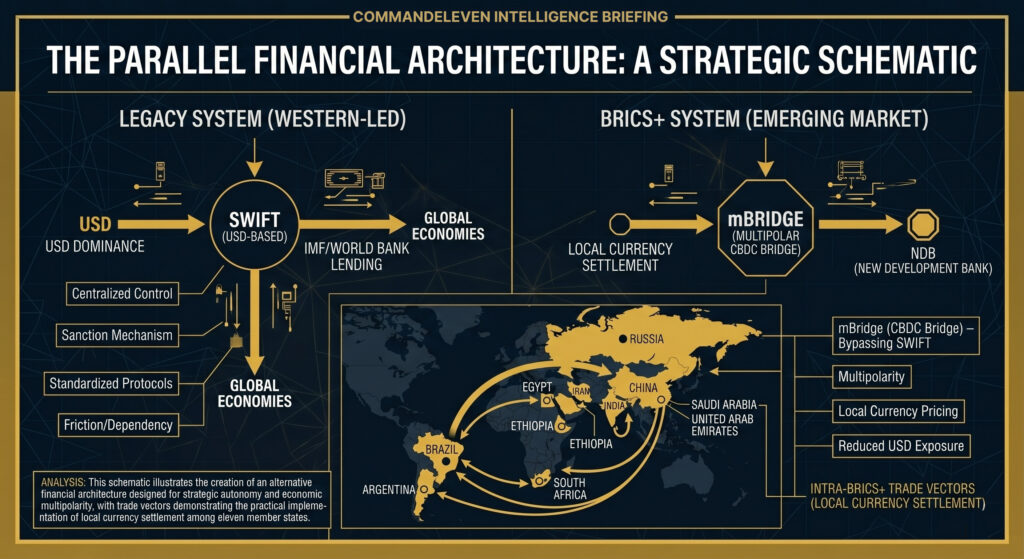

The mBridge and “BRICS Bridge” Infrastructure

The most potent tool of financial fragmentation in 2026 is the mBridge project,a wholesale CBDC platform for cross-border settlements.

- Bypassing SWIFT: Originally a BIS Innovation Hub project, mBridge has “graduated” to a fully functional autonomous platform following the BIS’s withdrawal in late 2024. It allows for local currency payments that bypass the US dollar and Western financial messaging systems like SWIFT.

- Volume and Dominance: As of early 2026, payment volumes on mBridge have reached approximately $55 billion (RMB 387.2 billion). While the digital yuan accounts for 95% of this volume, India’s 2026 agenda focuses on linking diverse national CBDCs to ensure the system is not dominated by a single member’s currency.

- De-dollarization Strategy: The “BRICS Pay” initiative focuses on retail and tourism payment linkages, enabling citizens to utilize national QR-based digital wallets (like India’s UPI or Brazil’s Pix) across the expanded bloc.

Strategic Autonomy and “Multi-Alignment”

The expanded BRICS is not a monolith but a flexible framework for “strategic multi-alignment.”

- Non-Ideological Cooperation: Unlike the G7, BRICS does not require full political or security alignment. For example, India and China continue to deepen financial integration via the New Development Bank (NDB) despite ongoing border tensions.

- South Africa’s Pragmatism: Pretoria has emerged as a key example of “middle-power” diplomacy, utilizing its BRICS membership to protect national interests in the Global South while maintaining vital trade links with Western markets.

- Resistance to Sanctions: The inclusion of Iran and Russia has institutionalized “sanction-proofing” as a core pillar of the bloc. By establishing independent insurance, shipping, and payment rails, BRICS members can conduct high-value commodity trade (oil, fertilizers, and minerals) without exposure to US secondary sanctions.

Institutional Challenges and Internal Divergence

Despite its rapid expansion, the bloc faces significant internal “friction points.”

- The Scale Problem: The admission of diverse economies like Ethiopia and Egypt alongside giants like China creates disparities in institutional capacity and credit fundamentals.

- India-China Rivalry: India’s 2026 Chairship emphasizes “interoperability” to prevent a China-centric financial order. New Delhi is wary of mBridge becoming a vehicle for yuan dominance and is pushing for a more balanced “public digital rails” model.

- Geopolitical Balancing: Regional powers like Turkey and Saudi Arabia continue to hedge their positions, maintaining NATO or US security ties while pursuing BRICS partner status to manage geopolitical risk.

Intelligence Assessment and Forecasting (2026–2030)

CommandEleven forecasts that the period through 2030 will be defined by the “Bifurcation of Global Capital.”

- Parallel Systems: We expect the creation of a “BRICS-centric” secondary market for private credit and commodities, operating entirely outside the dollar-dominated financial system.

- South-South Trade Liberalization: Trade between China and BRICS+ members is projected to grow by 5.5% annually, surpassing China’s trade with the US.

- Fragmentation of Global Governance: The G20 will likely diminish in relevance as the G7 and BRICS+ become the primary poles of global decision-making, each operating within its own regulatory and financial silo.